Cash Basis Or Accrual Basis Accounting

|

Wymiar: Nr katalogowy: |

Opis:

Accruals – What Are Accruals?

Accounting principles are the foundation of accounting according to GAAP. Record depreciation for a fixed asset over its useful life, rather than charging it to expense in the period purchased. Record revenue when you invoice online bookkeeping the customer, rather than when the customer pays you. Attach your profit and loss statement and balance sheets from the previous year to Form 3115. Include any adjustments you made to your books with the form as well.

Cash Basis Accounting Vs. Accrual Accounting

The cash method is allowed if the company has more than $1 million in sales and meets the service business test. ith the release of revenue bookkeeping procedure , the IRS provided small businesses with much needed guidance on choosing or changing their accounting methods for tax purposes.

Cash Basis Accounting

Cash accounting is the other accounting method, which recognizes transactions only when payment is exchanged. Accrual accounting is the opposite of cash accounting, which recognizes transactions only when there is an exchange of cash. Accrual accounting is almost always required for companies that carry inventory or make sales on credit. Patriot’s online accounting software is easy-to-use and made for the non-accountant. Accounts payable is recorded based on invoices during the normal course of business.

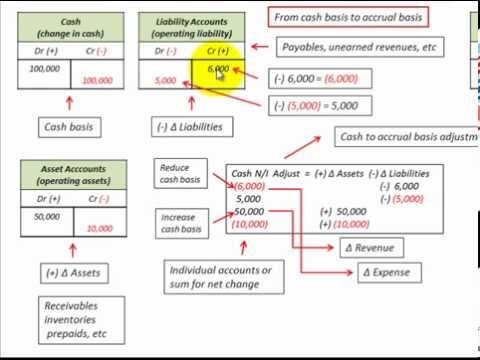

Diagram Comparing Accrual And Cash Accounting

It satisfies the requirements of major accounting standards applicable in the world such as generally accepted accounting principles (GAAP) and international financial reporting standards (IFRS). Now consider the following three cases in which John pays cash to Sam and records rent expense. If your business is a corporation (other than an S corp) that averages more than $25 million in gross receipts each year, the IRS requires you to use the accrual method.

Should A Small Business Use Cash Or Accrual Accounting?

Similarly, for obligations with monthly accrual rates, you would divide the annual interest rate by 12, and then multiply the result by the amount of the outstanding balance. But in extraordinary circumstances, such as during a period of negative interest rates, they might be negative. Accrual rates are often used to calculate the sum of paid sick time, vacation time, and pensions. An accounting error is an error in an accounting entry that was not intentional, and when spotted is immediately fixed.

The cash method is allowed if average sales are over $1 million but less than $5 million and the company meets the service business test. The accrual method is required if the entity fails both the $1 million average revenue and the material income-producing factor tests.

The exhibit below includes a flow chart to help small businesses select the proper accounting method. The accrual method is required if the company has more than $5 million in average sales. The accrual method is required if the entity fails both the $1 million and the material income-producing factor tests.

If you provide a good or service and invoice a customer, you gain a receivable. The invoice amount remains a receivable until the customer pays you. Save money and don’t sacrifice features you need for your business. If the phrase “accrued liability” is making you think that sounds complicated, don’t panic. An accrued expense is recognized on the books before it has been billed or paid.

There are several key differences between cash basis and accrual. Depending on which method you use, you recognize transactions at different times.

- An accrued liability is an expense that a business has incurred but has not yet paid.

- Payroll taxes, including Social Security, Medicare, and federal unemployment taxes are liabilities that can be accrued periodically in preparation for payment before the taxes are due.

- Accruals are revenues earned or expenses incurred which impact a company’s net income on the income statement, although cash related to the transaction has not yet changed hands.

- It provides an overview of cash owed and credit given, and allows a business to view upcoming income and expenses in the following fiscal period.

- Recording an amount as an accrual provides a company with a more comprehensive look at its financial situation.

If the average is less than the $1 million threshold, the cash method is always allowed (but not required). For purposes of this test gross receipts include most normal items, such as sales revenue, services, interest, dividends, rents, royalties and the like, but not sales tax the taxpayer collects. The term accrual is also often used as an abbreviation for the terms accrued expense and accrued revenue that share the common name word, but they have the opposite economic/accounting characteristics. Understanding the difference between cash and accrual accounting is important, but it’s also necessary to put this into context by looking at the direct effects of each method.

The accrual method is also required for tax shelters [IRC section 448(a)], and for general partnerships failing the $5 million test that have a C corporation as a partner (section 448(a)). Companies that are part of controlled groups must combine receipts for all entities included in the group to determine if they meet the $1 million test. For taxpayers in business less accural accounting than three years, the average is computed using revenue from only the years in existence. An employer pays its employees once a month for the hours they have worked through the 26th day of the month. The employer can accrue all additional wages earned from the 27th through the last day of the month, to ensure that the full amount of the wage expense is recognized.

A supplier delivers goods at the end of the month, but is remiss in sending the related invoice. The company accrues the estimated amount of the expense in the current month, in advance of invoice receipt.

Accruals are created via adjusting journal entries at the end of each accounting period. Accruals improve the quality of information on financial statements by adding useful information about short-term credit extended to customers and upcoming liabilities owed to lenders. Accruals are needed for any revenue earned or expense incurred, for which cash has not yet been exchanged.

Matching does not mean that expenses must be identifiable with revenues. You informed the IRS of your accounting method when you filed your first small business tax return.

When you fill out Form 3115, you report the section 481 adjustment. The 481 adjustment corrects issues with duplicating or omitting transactions during the transition. The section 481 adjustment reflects the changes you made to your books when switching from cash basis to accrual.

For example, a two-week pay period may extend from December 25 to January 7. At the same time, the accounting data is ‘bias-free’ https://www.bookstime.com/accrual-basis since the accounting data are not subject to the bias of either management or of the accountant who prepares the accounts.

Why is accrual accounting better than cash?

The accrual method is required if the entity fails both the $1 million and the material income-producing factor tests. The accrual method is required if the company has more than $5 million in average sales. The exhibit below includes a flow chart to help small businesses select the proper accounting method.

Employees may have performed work but have not yet received wages. Interest on loans may be accrued if interest fees have been incurred since the previous loan payment. Taxes owed to governments may be accrued because they may not be due until the next tax reporting period.

Cash receipts received during the current period might need to be subtracted. If a sale began in a previous period and you received cash in the current period, you need to reverse the sale in the current period and record it as a receivable in the last period (when the sale occurred). When you subtract cash receipts, adjust the current period’s beginning retained earnings.

Revenue procedure and the subsequent revenue procedure will not solve the cash or accrual questions that have plagued CPAs for the last 25 years. They are, however, a needed first effort at easing the https://www.bookstime.com/ recordkeeping and compliance burdens of small businesses. With the election of a Republican administration bent on tax changes, the likelihood of future increases in the sales threshold seems greater.

Every business has to record all its financial transactions in a ledger—otherwise known as bookkeeping. You’ll need to do this if you want to claim tax deductions at the end of the year. And you’ll need one central place to add up all your income and expenses (you’ll need this info to file your taxes). The cash method is also What is bookkeeping beneficial in terms of tracking how much cash the business actually has at any given time; you can look at your bank balance and understand the exact resources at your disposal. Accrual rate refers to the rate of interest that is added to the principal of a financial instrument between cash payments of that interest.